The UK’s Energy Mix: Changes, Trends & Future Outlook

Understanding the UK’s Changing Energy Mix

The UK energy mix is undergoing a significant transformation as the country moves towards a cleaner, more sustainable power system. Over the past decade, coal has been almost entirely phased out, while renewable energy sources now contribute more than 40% of the UK’s electricity. At the same time, total power generation has declined, driven by increased energy efficiency, onsite generation, and shifts in industrial demand.

UK Power Generation Trends: How Much Energy Are We Producing?

The UK’s total power generation through the national grid has declined by 20% since 2010 from over 325TWh to just under 260TWh. There are a few potential reasons for this:

- Onsite generation, for example solar panels, has replaced some grid electricity¹.

- Businesses and homes have increased energy efficiency efforts².

- The UK’s manufacturing output has also decreased during this time³.

How the UK’s Energy Mix Has Changed Since 2009

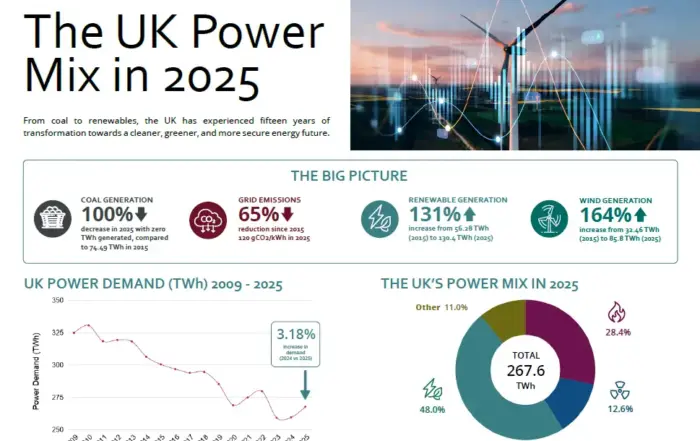

Looking at the chart, we can see that coal has been practically phased out with a huge reduction since 2019 and further reductions in 2023. Since 2009, coal production has decreased by 97%. In the last 12 months, only 1% of the UK’s power mix was produced by coal.

In regards to renewable energy, although it grew by nearly 110TWh between 2009 and 2022, there was some stagnation in 2023. Despite this, over 40% of the power used in the UK was from renewable sources.

Nuclear power has stayed relatively steady since 2009, with small decreases over the last 3 years, and is currently at just under 15% of the UK’s power mix.

‘Other’ power relates to the interconnectors we have, our imports from other countries like France or Germany. In 2023, this dropped slightly and currently under 10% of our overall power on the grid is from these other sources. According to a recent DUKES report, we actually became a net electricity exporter.

That leaves gas, the only significant flexible energy source. As coal is phased out completely, gas expectations will inevitably change year-on-year to meet the demand gaps once nuclear and renewables have contributed what they are able to. Currently, nearly 30% of our power mix is from gas production and whilst this is down from 40% a few years ago, we would expect this to continue to decrease as the tax on gas continues to rise, making it less attractive financially.

How the UK’s Energy Mix Affects Carbon Emissions

Scope 2 emissions from the electricity used from the National Grid are a factor of the generation mix and the demand for power. The higher emissions between 2009 and 2012 can be attributed to the mix of fuels on the grid. Since then, despite electricity use only declining by 20%, the changing mix of fuels has reduced Scope 2 emissions by 75%. More renewable electricity and less gas will help reduce this further.

Preparing for the Future

Over the next 5 years, it is anticipated that demand for electricity in the UK will increase from 325 TWh to 375 TWh, with it reaching as high as 600 TWh by 2050.

One of the main reasons for this increase is the planned removal of diesel and petrol cars for sale in the UK and those new vehicle sales being replaced by electric vehicles. The need to charge so many electric cars will inevitably push demand up. Other decarbonisation projects, such as heat pumps replacing gas boilers to provide us with our heating demands, and other ‘electrification’ projects will also contribute to this increased demand.

There is a continued expectation that onsite generation and renewable energy into the grid will continue to increase, as the need to reduce gas further becomes more pressing. We would predict renewable energy will likely be the ‘go-to’ as nuclear power plants will take more years to build than we have to reach net zero targets and there will be little appetite to rely on interconnectors.

What this means for your business

Over the next 25 years, we would expect businesses to be challenged to look seriously at electrification, either through the offer of grants and subsidies or by increasing the level of taxation on gas to make the business case stack up, or both.

We would also anticipate further renewable energy subsidies (for both on-site and grid connections) to grow renewable energy once again, and these subsidies will need to be paid for, probably through increased levies on energy bills.

Finally we would be prepared for some major changes around flexibility, storage, and pricing. As the UK gets to grips with a cleaner grid that doesn’t have the same levels of flexible supply as it once did, the responsibility for flexibility will be shifted to the demand side, either rewarding demand-side users for their flexibility (or punishing them for their lack of).

With these changes ahead, businesses should be prepared to mitigate risks and take advantage of any opportunities as and when they present. Businesswise Solutions stands ready to assist businesses in optimising their energy management practices, ensuring readiness for any significant transformations.

¹https://assets.publishing.service.gov.uk/media/66043298f9ab41001aeea3dd/Energy_Trends_March_2024.pdf

²https://www.iea.org/news/global-energy-efficiency-progress-is-accelerating-signalling-a-potential-turning-point-after-years-of-slow-improvement

³https://www.ons.gov.uk/economy/economicoutputandproductivity/output/bulletins/indexofproduction/january2024

Connect with us

Want more insights like this? Sign up for EnergyIntels and stay informed with the latest industry updates.

More From EnergyIntel

How One Manufacturer Turned Energy Into a Board-Level KPI

EMaaS in Action: How One Manufacturer Turned Energy Into a Board-Level KPI Every manufacturer knows energy is a significant operational cost, but understanding where it's really being used [...]

UK Power Generation Mix in 2025

The UK Power Mix in 2025 How the UK’s electricity system has been transformed Over the past 15 years, the UK electricity system has undergone one of the fastest [...]

Technical Energy Cost Structures and Their Impact on Energy Strategy

How Technical Energy Cost Structures Are Redefining Energy Strategy When boards turn their attention to energy, the conversation almost always begins in the same [...]