Nuclear Regulated Asset Base (RAB): What you need to know

The UK government is introducing a Nuclear Regulated Asset Base (RAB) scheme to fund future nuclear power developments, starting with the Sizewell C site in Suffolk. A Final Investment Decision has now been made for the project, with the construction cost revised to £38 billion, a significant increase from the original £20 billion estimate. The government has an initial 44.9% share in the development.

The scheme is intended to fund the full lifecycle of new nuclear projects — covering design, construction, commissioning, and operation. It shares similarities with the Contracts for Difference (CfD) mechanism, which could see the scheme being a benefit as well as a cost once a nuclear site is generating energy. The RAB marks a fundamental change in how nuclear projects are financed, shifting some costs onto consumers during the construction phase, rather than after generation begins.

From 1 November 2025, the RAB levy will start appearing on all energy bills at a rate of £3.46/MWh, rising to £3.93/MWh from 1 January 2026.

Purpose and structure

The RAB model allows developers to recover costs during construction rather than waiting until the project is complete. This lowers financing risks, reduces reliance on public borrowing, and is designed to encourage private investment into nuclear projects.

However, the approach transfers some risk to consumers, who begin contributing to costs before receiving any energy. If projects overrun in time or budget, household and business bills may rise beyond initial estimates.

How does RAB differ from CfD?

While the RAB shares similarities with CfD, the timing and risk split differ significantly:

| CfD | RAB | |

|---|---|---|

| When consumers pay | Once generation begins | During design and construction |

| Financing risk | Higher (borne mainly by investors) | Lower (shared with consumers earlier) |

| Bill impact | Only after operation starts | Upfront, before power is delivered |

This makes nuclear projects more investable by creating a stable, predictable funding model, but it also introduces upfront consumer costs.

Rate information

At this stage, early modelling suggests a potential impact of around £1/month on domestic energy bills during the 9–12 year construction period. This translates to an estimated £4 per MWh, assuming a consistent unit rate across usage types.

Broken down, this looks like +0.3455p/kWh on consumption from November 2025 (about a 1.7% increase on a 20p/kWh delivered price), and +0.393p/kWh from January 2026.

How costs will be phased in remains unclear, though the government has already provided financial support to Sizewell C to avoid a standing start. Once the site is operational, the funding structure will pivot toward a more familiar CfD-style arrangement, offering price certainty for the energy generated.

Who pays and who manages

Consumers: Households contribute via a levy on bills, with a greater proportional burden on energy-intensive businesses.

LCCC (Low Carbon Contracts Company): Manages revenue collection and distributes funds.

Ofgem: Provides regulatory oversight, ensuring costs recovered through the RAB are efficient and justified.

What this means for business energy contracts

At this stage it is important to note that it is still unclear how suppliers will recover this charge from customers. Unless your business energy contract is fixed, suppliers have the right to pass on these charges.

The way RAB affects your bill depends on your supply arrangement:

In practice, this means businesses on flexible arrangements should plan for charges from November, while those on fixed deals should review contract terms to understand supplier rights.

Wider policy context

The RAB model is intended as a template for future nuclear developments, not just Sizewell C. It is central to the UK’s strategy to achieve up to 24 GW of nuclear capacity by 2050, underpinning both the government’s net zero commitments and energy security strategy.

By reducing reliance on imported fossil fuels and balancing intermittent renewable sources, nuclear is expected to play a stabilising role in the energy system for decades to come.

It is expected to be included in carbon tax exemptions, though this has yet to be formally confirmed. If exempt, costs would be redistributed to non-exempt users, creating further knock-on impacts.

Timeline and risks

Risks include potential overruns in construction. If costs escalate, consumer contributions may also rise beyond current estimates.

Stakeholder impact

How to mitigate the impact

The RAB charge is consumption-based. Unlike some other non-commodity charges, there is no benefit from shifting usage to different times of day. The only way to reduce exposure is by reducing total energy consumption.

This makes efficiency projects and carbon reduction measures more important than ever, not just to cut emissions, but to protect against rising non-commodity costs.

Talk to our experts about strategies to offset rising non-commodity costs.

Connect with us

Want more insights like this? Sign up for EnergyIntels and stay informed with the latest industry updates.

More From EnergyIntel

How One Manufacturer Turned Energy Into a Board-Level KPI

EMaaS in Action: How One Manufacturer Turned Energy Into a Board-Level KPI Every manufacturer knows energy is a significant operational cost, but understanding where it's really being used [...]

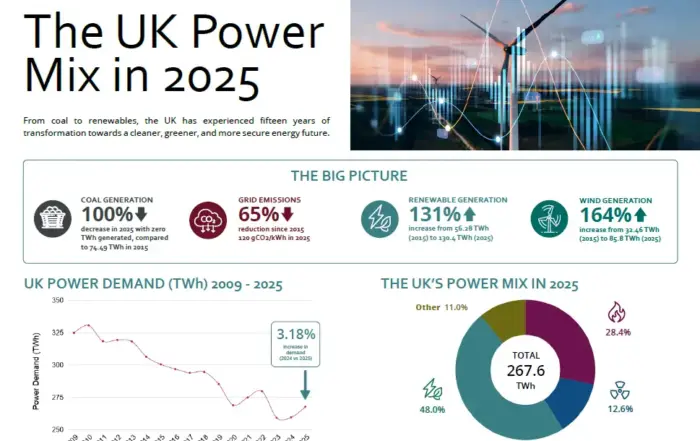

UK Power Generation Mix in 2025

The UK Power Mix in 2025 How the UK’s electricity system has been transformed Over the past 15 years, the UK electricity system has undergone one of the fastest [...]

Technical Energy Cost Structures and Their Impact on Energy Strategy

How Technical Energy Cost Structures Are Redefining Energy Strategy When boards turn their attention to energy, the conversation almost always begins in the same [...]